CeFi: Centralized Finance

The use and knowledge of cryptocurrencies around the world it’s not a new topic anymore, like it was a few years ago, right now a lot of people have an ordinary understanding for different motivations like: curiosity, constant exposure on social media, legal frameworks of some countries or just for simple greed. In the past, there was a negative feeling about these technologies, probably for the lack of knowledge, but now, it is common to see various kinds of people involve, from extremely poor people to big companies. However, if we make simple research about other projects, we can conclude that cryptocurrencies and first generation of blockchains are not the top of evolution, cryptocurrencies and other tokens are simple tools to access to other types of financial services more novel and complex. Since the beginning of crypto space centralized intermediaries better known as CeFi facilitates financial services that in some sense replicates the ones that we can find in TradFi, but at the same time CeFi has created new kinds of crypto services that does not exist in traditional finance, of course, with all the security risks and legal uncertainty proper of this ecosystem. In this regard, critics of CeFi claim, why do people use these crypto services if they are so risky? Don’t they know that in traditional finance already exist digital services related with fiat, commodities, stocks, and many others that comply with security and legal standards? However, TradFi enthusiasts do not realize that all these kinds of services are not available for a lot of people in the world. CeFi platforms grow rapidly, it is easy to access them and their functions are important, they facilitate the use of cryptocurrencies, but at the same time, often face critics about their inherent centralization, cybersecurity risks and legal uncertainty in most countries. From a legal perspective CeFi infrastructure it is similar to traditional finance, at least in develop countries, on the other hand, it is not a secret that undeveloped countries do not have a functional legal structure in most areas, for that reason to organize and regulate CeFi will be a big challenge. Right now, we can observe that strong governments and some international organization have an aggressive policy to organize CeFi, specially in financial and tax compliance. This situation generates different opinions, some critics claim that an abuse of regulations will affect the evolution of these technologies, on contrary; regulators say that it is important to fix boundaries to protect users and investors. In this sense, it is very fascinating that just when we started to see more legal actions against crypto intermediaries, DeFi space begins to have more development and importance.

DeFi: Decentralized Finance

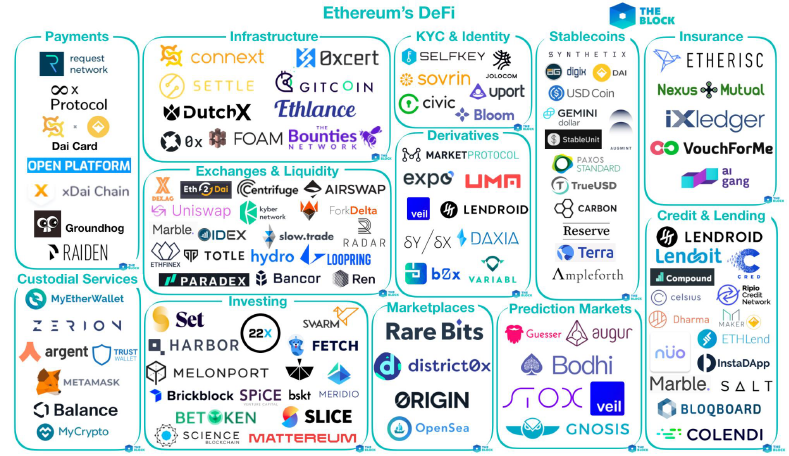

DeFi initially called Open Finance pretends to create a new digital financial system, who can be used by any person in the world just with an internet connection, one of the goals of DeFi is to replicate all the traditional financial services that we know, but without the need of a company or centralized institution, at the same time, DeFi pretends to create new financial services, more novel and complex, DeFi refers to new financial tools that are manage thanks to decentralized code develop in a public blockchain. Some experts claim that the only and first DeFi was Bitcoin, thanks to characteristics like independence and freedom in the transmission of value, on contrary, others think that the creation of a new financial system it is not possible to develop only with the bitcoin token, a modern society requires different types of decentralized services like credits, lending and borrowing, insurance, payment networks, stables assets, financial derivatives and many other services. In 2014 Bitcoin inspired the creation of Ethereum, a public blockchain that allows the development of decentralized applications, some of them DeFi projects. Evolution: DAI a stablecoin collateralized initially with Ether, was one of the first DeFi projects, later in 2017 the ICO phenomenon took place, a big part of the ICOs launched were frauds or failed projects, however, some ICOs achieved to finance some DeFi platforms that were the basis of the ecosystem. The main characteristics of DeFi are; pseudo anonymity, transparency, permissionless and non-custodial of asset by any third party. DeFi works thanks to smart contracts that are programs develop in a blockchain, DeFi in Ethereum represents different layers of innovation that permit the construction and interaction with decentralized finance. Ethereum has its own native token, better known as Ether, at the same time Ethereum allows the creation of other token standards like fungible tokens, non-fungible tokens, and many others. When we think about Ethereum and DeFi, the first topic that comes to our mind are decentralized exchanges DEXs and lending platforms, these DeFi services are the most common at this stage, but there are many others categories and tools who help these technologies.

Source: http://www.theblockcrypto.com

The idea of a new collaborative financial system with global access is fascinated, having access to services that constantly evolve creates a new hope for a better and more inclusive world, this expectation is not too far, right now some DeFi platforms work well and, in some cases, they are extremely helpful, but not everything is positive, there are some limitations, uncertainties and deficiencies that needs to be fixed, if the intentions is to create a functional decentralized system. Ethereum is the blockchain that has more DeFi platforms, also is the most popular blockchain, for those reasons it is common that the network is saturated, this situation affects the cost of transactions which are extremely high at this moment, at least from the view and experience of common users. Right now, we can observe different proposals and some upgrades that pretend to solve this situation in a short term. Another limitation to count is the complexity of DeFi activities, we can observe a lot of technical practices and new concepts that can confuse users, for those reasons a constant education, investigation and experimentation are an obligation for all the people involved not only in DeFi but in all blockchain practices.

Like any other digital practice, the blockchain ecosystem and in this case DeFi is also exposed to risks not only in terms of IT security, but also economic risks. From an IT security perspective, the smart contracts, which are the backbone of every DeFi tool, can manifest deficiencies, errors or vulnerabilities that result in malfunction or in the worst case in the loss or theft of funds. From an economic perspective, exposure to market manipulation techniques is present and many criticize the design of the governance system of each service, so far we have observed that most DeFi protocols whatever their nature (decentralized exchangers, lending, stablecoins etc. ) operate in the form of digital communities, as is usual in blockchain, therefore, decision making being decentralized in nature, does not depend on a central body, but users express their will through votes based on the project tokens they own, which is criticized, since obviously concentrations of power can arise from those who own more tokens and decide to give a negative direction to the project that affects the interests of the other participants, without forgetting the new and complex modalities of scams that are emerging. DeFi is in constant construction and evolution, it is naive to think that it is already consolidated, trial and error is the common denominator in many projects.

Like any other digital practice, the blockchain ecosystem and in this case DeFi is also exposed to risks not only in terms of IT security, but also economic risks. From an IT security perspective, the smart contracts, which are the backbone of every DeFi tool, can manifest deficiencies, errors or vulnerabilities that result in malfunction or in the worst case in the loss or theft of funds. From an economic perspective, exposure to market manipulation techniques is present and many criticize the design of the governance system of each service, so far we have observed that most DeFi protocols whatever their nature (decentralized exchangers, lending, stablecoins etc. ) operate in the form of digital communities, as is usual in blockchain, therefore, decision making being decentralized in nature, does not depend on a central body, but users express their will through votes based on the project tokens they own, which is criticized, since obviously concentrations of power can arise from those who own more tokens and decide to give a negative direction to the project that affects the interests of the other participants, without forgetting the new and complex modalities of scams that are emerging. DeFi is in constant construction and evolution, it is naive to think that it is already consolidated, trial and error is the common denominator in many projects.

CeFi Legal Challenges

Traditional finance in most jurisdictions is one of the most regulated sectors, the trend is increasing, this same path awaits cryptocurrency intermediaries, what initially aspired to be independent, autonomous, and decentralized may turn out to be much more centralized and regulated than the traditional, at least in some countries, this for obvious reasons, an entity with fully identified legal personality will be under constant harassment by auditors and regulators. Regulation is important because it generates trust, protection, order, and legal certainty, if it is conscientiously developed by qualified subjects and implemented by credible institutions, otherwise, it is only more bureaucracy, regulatory saturation, and the rest of the already known evils that the blockchain movement criticizes so much. Not all countries have and will ever have the capacity to regulate and oversee CeFi, the most notorious disputes and criminal activities are highly likely to be investigated and resolved thanks to the intervention of international digital oversight bodies, in fact, we are already seeing it. In the context of decentralized finance, the challenge of regulation and oversight rises to another level, in principle DEFI simulates highly regulated financial practices, when this situation becomes evident, the immediate reaction of regulators will be to try to organize or in the worst case destroy this ecosystem, however, the following questions arise Is it possible to regulate DeFi? Is it possible to regulate financial practices developed within decentralized databases?

DeFi Regulatory challenges

It is complicated to give a simple and absolute answer, many factors must be taken into account, this paper raises the basic and most obvious questions, a specific regulation would have to break down and classify each of the DeFi services, i.e. regulations for DEXs, decentralized stablecoins, lending/borrowing and any other novel service that may arise, it would also have to be analyzed in which type of blockchain it operates and how it works, as there are definitely platforms some more decentralized than others.

The first challenge that comes to mind is that there is no central authority to subject to legal norms, traditional legal systems are experts and are used to regulate and control intermediaries, but what happens when complex financial practices occur exclusively within a decentralized code with global access. To whom to establish obligations? To the programmers and developers, some of them are anonymous or are in countries with legal advantages to carry out their activities, others have a lot of prestige and popularity, however, they only develop the bases of the code which is later released and begins to evolve like any other open-source code which becomes part of a large community. There are projects that presume to be DeFi, however, have a high influence and control of a small group of people, perhaps in this mode is more feasible to regulate and control, in this order of ideas, begins to emerge some distrust about the intention to criminalize the inventive and creative activity of programmers, Although it is more than evident the existence of highly trained individuals who use their knowledge to commit crimes, it is also important to encourage and protect the technicians who dedicate their lives to find and solve global financial problems.

The intention could be to regulate and hold the holders of DeFi platform governance tokens accountable, since they are the ones who make the decisions on the direction of the project. The problem is that in the absence of a central issuing entity, it is difficult to identify the holders, obviously they can be traced by means of chain analysts, but these would surely be distributed in different geographical locations, not to mention the use of anonymizers, therefore, a specific legislation would have authority only over the token holders located in their jurisdiction. One way to identify governance token holders is on the assumption that they deposit their assets within centralized intermediaries in case they wish to exchange them, however, they also have the option to do so through DEXs. Some jurisdictions, in an attempt to curb this evolution, may implement radical measures by prohibiting regulated intermediaries from entering tokens from DeFi protocols, as is already the case with some privacy-focused tokens. What we do see today is a greater requirement in procedures such as the travel rule, which implies a full identification of the origin of the transaction, therefore, it is important to have the necessary arguments to justify the origin of tokens linked to decentralized finance, currently some Blockchain projects begin to generate reports to facilitate this task to users who wish to enter their tokens within intermediaries. However, a fundamental point to consider is that many DEFIs operate through DAO’s this for reasons of information security and transparency in governance, territories such as Wyoming already regulate this variant of digital social organization, so there we could begin to observe some inclination of regulation operating through this model in specific territories, we find similar uncertainties when trying to regulate the users of DEFI platforms.

This type of decentralized practices brings back the issue of legal universality, since DeFi rules will definitely arise in some jurisdictions, certainly in those more developed ones, but these provisions will be limited only to the citizens of those nations and to the users of centralized stable coins collateralized with fiat or token holders linked to the regulated territory, for such reason, it is likely that proposals for uniform rules applied by several countries simultaneously, or treaties or international bodies promoting or imposing regulations in the same sense for members, will emerge, this as an attempt to solve problems such as the applicable jurisdiction, which is another of the great challenges not only of DeFi but of blockchain in general.

The blockchain evolution has been characterized by following a diverse path, that is to say, there is no specific roadmap to follow, each project follows its own course and in that path finds a user base, therefore, there are projects that aspire to absolute decentralization and move away completely from traditional systems, on the contrary, others seek to integrate the consolidated centralized with these new variants, For this reason, it is likely that both cryptocurrency intermediaries and some traditional financial institutions will incorporate to their services some modalities related to decentralized finance, which will bring legal uncertainties, but will be more assimilable.

Financial and tax compliance

In terms of financial compliance, a topic that will always be present is the prevention of money laundering, again the question arises: Who to submit to these rules or AML recommendations? It is clear that there is no central entity that applies them and generally there are no directors or owners that are responsible, but only a code to which everyone has access. This topic is quite specific so it should be expanded in the future, as a first impression, certain concerns arise about the illicit origin of some tokens that enter DeFi services, to understand the magnitude of the uncertainty it is important to be clear about the operation of some DeFi as DEX or Lending, without going into further details, these services to carry out their activities need liquidity, i.e., need tokens to exchange or lend, These assets are obtained from the contribution made by individuals to the protocol (liquidity providers) motivated by certain economic incentives, once the tokens are deposited to the service (Liquidity Pool) different technological principles are applied, mathematical formulas, smart contracts that achieve that common users use the service in a decentralized way, thus contradicting the operation of centralized entities both cryptocurrencies and traditional finance. The main concern is that tokens coming from illicit activities are contributed to these services, with the intention of mixing or laundering them.

The FATF Financial Action Task Force in the recommendations of the year two thousand nineteen, understands the existence of financial decentralized applications that do not have identified administrators, however, suggests that in those cases where there is an owner or operator of a decentralized application (DEFI) these could fall within the definition of a Virtual Asset Service Provider VASP, these recommendations do not provide further details on the form of incorporation and control within a jurisdiction, additionally questions arise related to what was exposed in previous paragraphs about the uncertainties between centralized legal compliance and blockchain, even so, this measure is one of the first steps to try to establish criteria for the prevention of money laundering. In the year two thousand twenty-one there was a high expectation about new FATF recommendations, which were speculated to bring concrete recommendations, although these were issued, they do not contain specialized measures, except for some definitions and merely conceptual aspects related to financial decentralized applications, however, it is emphasized again on what was indicated in the year two thousand nineteen, DEFI software is not a VASP, but its creators, owners, operators and other persons who maintain control or sufficient influence may fall within the definition of a VASP.

The DeFi tax issue maintains the same questions as cryptocurrencies, some countries already have some tax organization on native cryptos, in the case of DeFi tokens that enter intermediaries located in countries already organized, they will simply be subject to the established tax laws, however, we must not forget the classification of tokens, since not all represent the same thing, in DeFi we can be dealing with tokens of very different nature and characteristics for example: native cryptocurrencies, tokens collateralized with; fiat, metals, other cryptocurrencies, or tokens representing some underlying value such as synthetic tokens that track the price of an asset or real world financial derivatives, tokens representing physical or intangible assets, governance tokens, rewards, access rights etc. Tax compliance varies from jurisdiction to jurisdiction, in principle each legal system should have criteria on the different taxes applied to each of the existing token variants and at what times the tax liability materializes. Obviously, there will always be individuals who seek to take advantage of DeFi to avoid or evade the rules in force. On the contrary, countries that continue to have uncertainties about the tax treatment of cryptocurrencies now have more unanswered questions. It is precisely in these issues where jurisdictions such as El Salvador draw attention, since all this complexity and tax confusion can be resolved by simply exchanging any token of value to Bitcoin thus taking advantage of the tax exemptions of the aforementioned country.

DeFi in Guatemala

Guatemala does not have a legal position regarding native cryptocurrencies, which is positive or negative depending on the perspective, therefore, there are also no special rules regulating financial practices within decentralized and global databases. This situation brings to the table the debate on the scope of application of Guatemalan law, since some consider that certain interactions within cyberspace exceed the competence of the State, on the contrary, others defend the idea that all activity developed by persons located in Guatemalan territory are subject to national laws, regardless of whether their acts have a consequence in the physical or virtual world. If the first criterion prevails, there is not much to discuss, everyone who participates in DeFi is isolated from Guatemalan norms, if the second criterion prevails, DeFi developers and users have many rights and freedoms just like any other citizen, however, the obligations are uncertain, for this reason, the State does not regulate DeFi, but it does guarantee different constitutional rights that are related to these practices. For example, developers and users are assisted by constitutional guarantees such as freedom of action, freedom of industry, commerce, labor, digital private property, freedom of association in the form of digital communities or new forms of digital social organization, as well as the right of authors and inventors who enjoy exclusive ownership of their work or invention, which includes the creation of a token that represents value, digital art, or software. Every right or freedom will always have a limit, they are not absolute attributions, such limits are found in the current legal system, in the case of DeFi we do not observe specific limits, even so, the developer and user must always verify that their activities do not transgress any national law, it is unlikely that activities that are developed exclusively within distributed databases transgress the rules so far in force, however, when these activities transcend the digital to the physical and regulated world, for example, the relationship with national currency, in that case definitely apply all relevant laws. Other limits to the freedoms described above are not to transgress morality or good customs, which in this digital environment is quite subjective to determine.

The civil and commercial contracting linked to DeFi is justified by principles such as freedom of contracting, autonomy of freedom and the perfection of contracts by simple consent. As it happens with cryptocurrencies, there may arise individuals or legal entities offering DeFi services to individuals, with the intention to mislead, confuse, or in the worst case to defraud, an individual or legal entity cannot offer DeFi services, as we indicated in previous paragraphs the nature of DeFi are financial services that operate in distributed databases, Any individual can have access to them, there is no need to ask permission or authorization to third parties, therefore, these practices are not linked to a company or a centralized person, if an entity or individual offers financial services under the slogan DeFi, that will be any other variant but decentralized finance. This brings us to the issue of user and consumer protection, making it clear that there is no legal protection for Guatemalan users involved in these activities and probably never will be, if a subject located in Guatemala acts as a liquidity provider, user, holder of governance tokens etc. of DeFi protocols and this is compromised, there will be no national entity to claim responsibilities, the only way, for now, will be to seek help within the global community of the specific protocol. The common thing to do if you have a problem or doubt, is to turn to the communication channels of the service, such as social networks like Discord, which is worth warning, in these media can also roam ill-intentioned subjects who seek to take advantage of the poorly informed. In the future we will see more cases of failed DeFi projects, which will serve as experience to learn to deduce responsibilities. From the studies and research that this author has done, some advances can be observed that can achieve transparency and efficiency of DeFi, for example, the implementation of decentralized digital identities, this from the perspective of greater transparency and efficiency for the benefit of users.

It is evident that some liquidity pools that require tokens from individuals to carry out their functions by means of smart contracts, what they are doing is capturing assets from the public, a practice better known as financial intermediation, which requires licenses and legal authorizations in practically the whole world, When this is carried out by decentralized platforms it will be quite complicated to enforce compliance with them, for the arguments already exposed, on the contrary, when protocols arise where the dominance and influence of a group of people is more evident, the deduction of responsibilities and the obligation to legal compliance will be more notorious, however, it will depend a lot on the geographical location of the holders. These aspects must be clear to the Guatemalan digital entrepreneur who wishes to lead an initiative of this nature, since in our country the crypto issue is quite uncertain, and much more, decentralized finance, so you must be fully aware of what you are doing.

Final thoughts

One of the most common observations of individuals towards DeFi is that these practices imply an exclusive relationship with blockchain tokens, for many this is a parallel digital world, crazy, tiny and only for experts, therefore, physical goods and traditional financial practices do not apply to these digital variants, one and the other are opposites have nothing to do. These assessments are wrong, since we are currently in a tokenization process, which allows linking virtually every human good to a blockchain, obviously when a real world good is tokenized it generates a direct relationship with the legal system in which it is located, as we indicated above, regulations in this sense will surely arise in some countries, on the contrary, it is clear that the rest of underdeveloped nations, with exceptions (perhaps El Salvador), are unlikely to adapt in the short term, However, we must keep in mind that individuals, regardless of their geographical location, have free access to all existing DeFi and tokens, therefore, we will surely observe the emergence of secondary markets that allow access to tokenized assets located or issued in specific jurisdictions, which is positive, but also forces the holder to find out if there are legal obligations in other countries that may bind it, on the contrary, if the DeFi and related tokens are decentralized in nature, the legal uncertainty will remain present.